A poor man is the one without a dream and a plan.

Be fearful when others are greedy, and be greedy when others are fearful. - Warren Buffett

Warren is telling you to buy low, sell high in the crisis

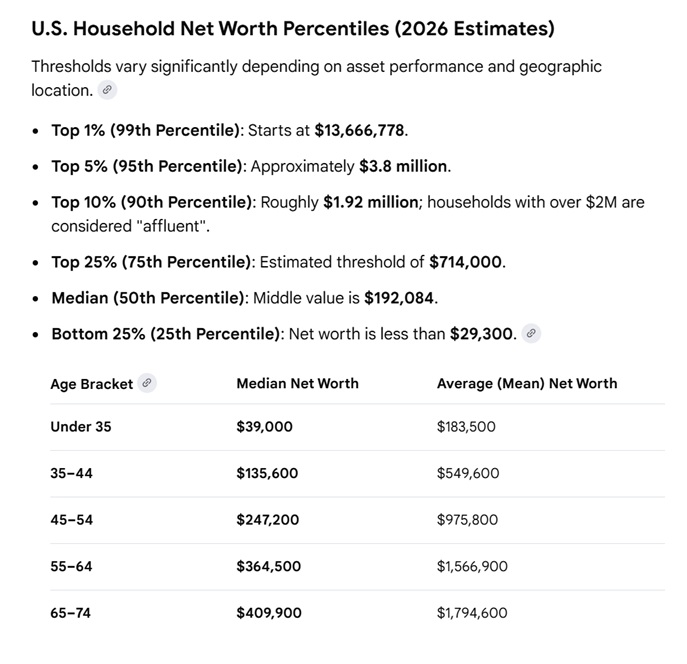

It does not matter how much money you have, your behavior builds legacy. The four pillars of successful wealth management are: knowledge, intelligence, independent-thinking and discipline. Historically the people who managed to rise up above crowd are A) has the ability, B) sees the opportunity and effectively uses it, C) plus a little luck of the time and destiny. True success is not measured by wealth, status, or personal achievements, but by how those achievements impact others, promote greater good. It emphasizes purpose over possession beyond self-centered toxic traits. The real value of success is in uplifting people, inspiring growth, and creating positive change in society. It reminds us that generosity, kindness, and contribution define a meaningful life. Ultimately, what matters most is the legacy we leave behind. | I am grateful I came to Rice U. with 1st-year full scholarship stipend and tuition-free, 2nd-year on as on gradute studant stipend working for Dept. professors. My full-time engineering-jobs companies paid for tuition with my own full effort to earn a MBA degree from Univ. of Houston University-Park. I am now giving back my free service to the local society.

Volunteer free service for the underprivileged:

Tennis advisor

Health advisor

Financial management advisor

Career advisor

A minister told the following story:

A pastor in a church experienced a 500-years flood. He believed God will save him and his church. He did not leave. Police came ordering evacuation, he did not leave. Firemen came to rescue, he did not leave. Even Army came with a boat, he did not leave. He was drowned. |

I am grateful to the great Professor Dr. Kenneth Eugene Lehrer and other professors in Dept. of Finance at UH MBA program in the early 90's. Kenneth is a PhD from NYC and was a Chief Financial Officer before. Tough as he seemed when he spoke (he is New Yorker), he taught us everything about the stock market, real estate, economy, goverment (Fed Central Bank) and financial management. He taught us from his real-life experiences and what learned from the [Economist] publications etc. I learned tremendously on every complex subjects from Kenneth. He seems enjoy teaching a student who has so much enthuism. This learning adds tremendour value to my lifetime in wealth management. Peter Lynch and Warren Buffet both had said: "You should not be buying something you do not understand". We may not have big talent like them, we could have smaller talent to make next level of riches. Investment instrument each ticker is just a product on financial market. Understand what that product does for you and how, before you buy it.

I have been investing in stocks and ETFs since graduation with MBA 1994 starting with mutual funds for first 4-5 years, then trade commmon stocks trying [Wall-Street fund-manager experiences] for 6-7 years, transitioning into developing market ETF because US crash went into lost decade for 6-7 years, then back to USA ETF Index funds for 15-17 years. I made quite a sum of money in a way safe within my mixed portfolio. I always say there are two laws in wealth management are much like |

|

BehaviorStrategyThe purpose of diversification is to make sure when you need money you don't incur too much loss "sell low" or "wiped-out" at down turn. Diversification of risk/reward mitagates up-n-down impacts. Diversification means you choose a targeted allocation by your realistic goal on a balanced risk-reward investment structure. Diversification is an equalizer.If your foreseeable expenses are covered by liquid asset, fixed income, savings, stable commodities etc., your untouched long-term investment should be in technology. We saw tech booms, like PCs in the 80's, Internet in the 90's, eCommerce, mobile in the 2000+'s, social media, cloud, streaming during and after lost decade tech bubble burst and subprime mortgage crash, then the fruits of eComm and now AI budding. In the long run, if you can hold out investment equity, it will gain for you. It is just the timing we do not know. If you enjoy the thrill, you can have a small portion X percent on the ultra risky instruments - you could be lucky to hit 10+ baggers or lose the high risk investment all. Semi-conductor sector demand doubles every 5 years, why cannot you 2X your ownership-equity every 5 years? This is a very logical thinking. The remaining part is your execution. It is too hard to pick a particular company, even pro cannot predict future. It is wise to hold a few non-leveraged ETF baskets (depends on your realistic goals, strategy and appetite - too greedy can drown you, too unambitious can starve you). You can use my 80-20 allocation strategy at below the bottom of this page. When the market eventually back to equilibrium (be after boom or crash) ETF is a balanced collection of equity that is not too crazy, diversified with multiple stocks either in one sector or total market, low expense, less fees and tax. If you have covered immediate living expense cash-flow thru short-term up-and-down, you can hold tight in bust-cycles or even buy more shares, and enjoy harvest on boom-cycles. |

I don't invest on risky asset such as swap at all but to show you an Example: Equity index swap(Let me explain here: in a down-turn crash, investor could be belly-up fast having to pay fixed contract rate + index negative return. In the case of below USD example, it is 2 times faster due to 2X leverage effect.) |

| Example of Proshares: The ProShares Ultra Semiconductors ETF (USD) is a leveraged exchange-traded fund that uses swaps and other derivatives to achieve its investment objective, it uses index rate in contract but is not an index fund. The fund seeks daily investment results that correspond to two times (2x) the daily performance of its underlying benchmark, the Dow Jones U.S. Semiconductors Index. How the Swap Mechanism Works Underlying Index: The ETF tracks the Dow Jones U.S. Semiconductors Index, which includes major chipmakers like NVIDIA, AMD, Intel, and others. A total return swap is a contract with a bank or financial institution. The ETF pays the bank a financing rate (interest). In return, the bank pays the ETF the daily performance of the semiconductor index multiplied by 2. By the multiplier, in an up market bank keeps losing money, speculators keep pouring in money to buy shares; in a down market ETF will lose all equity. Somebody has to pay for the risk - I assume this is the arm of investment banks that regulations allow more risky operations. That is why so dangerous. The bank or ETF can be bankruptted due to the realized risk to a level. Since USD only has about half in underline stock market security, SIPC is not protecting the other half.

|

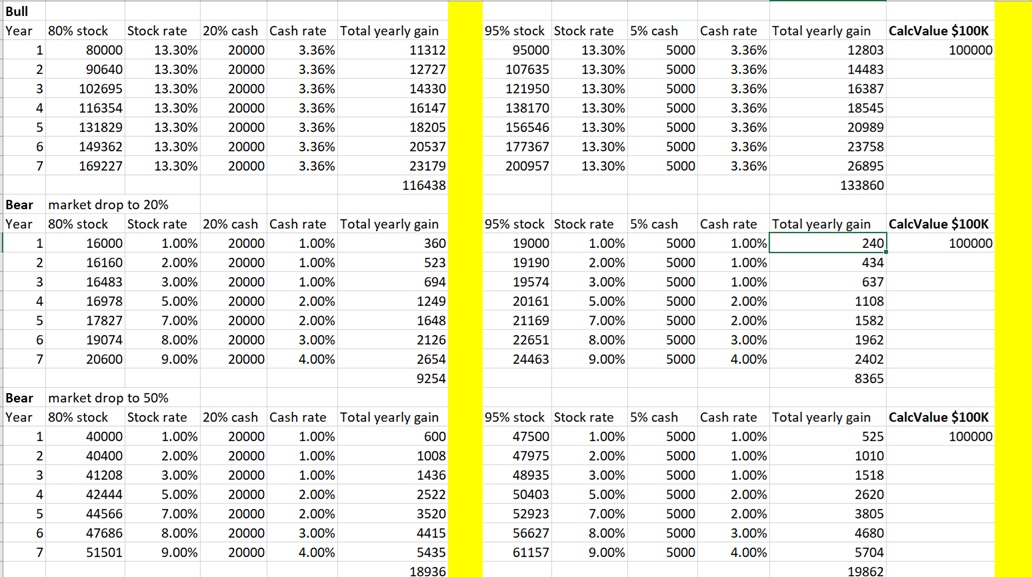

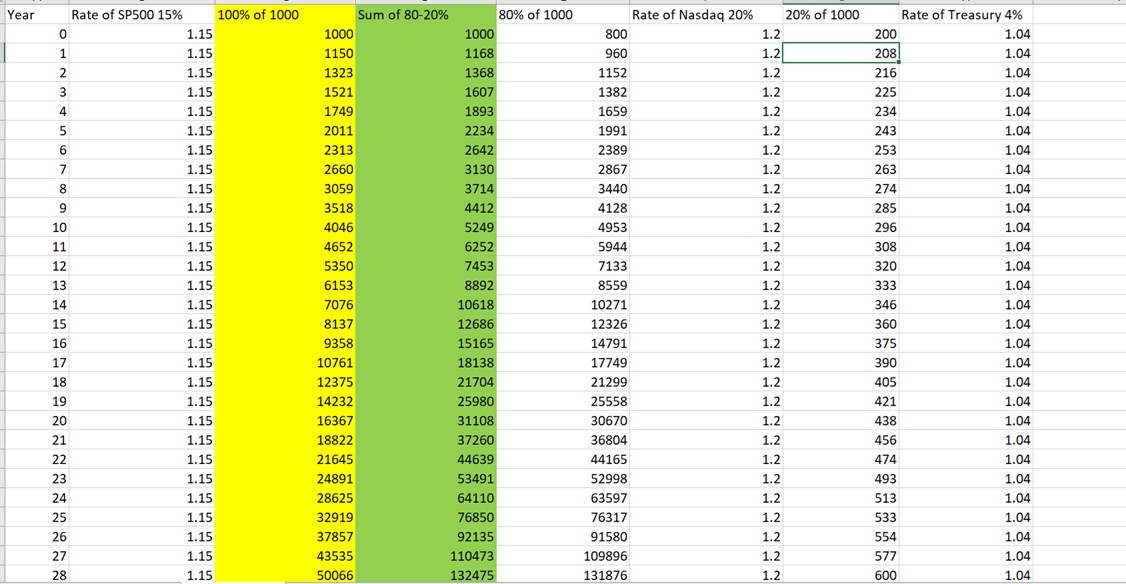

| 1st chart Bull-Bear 80-20 analysis and 2nd chart Bull market 80-20 for a number of years: |

|

|